Prefer to Listen? Play this quick summary instead!

The financial impact of a workplace injury is often felt before the medical picture is fully understood. Income may stop immediately, treatment begins quickly, and administrative requirements follow just as fast. In that early period, uncertainty around weekly payments can become as stressful as the injury itself.

For injured workers and families, a clear understanding of the structure makes the process easier to manage. It also helps explain why claim progress, payment timing, and payment amounts can change over the life of a claim.

At AusRehab, much of this uncertainty appears in practical form. This article addresses common questions about the commencement of income support, payment variations, and insurer requests for additional information.

💡 Quick Answer

In NSW, provisional weekly payments will usually begin within 7 days where the insurer has been notified, and entitlement is established. Payment commencement can occur before the insurer reaches a final liability position. Timeframes often depend on the quality of the information available at the beginning of the claim. Payment amounts can also change as the claim moves through different statutory periods.

How Long Does WorkCover Take to Pay?

The early payment process is designed to reduce financial strain while the insurer assesses the claim. That means a worker may begin receiving weekly payments while liability is still under review. Payments can start before the claim is fully approved.

Much of the timing comes down to documentation. A current certificate, clear injury details, and accurate earnings information give the insurer a better basis to start payments without avoidable delay.

A reasonable excuse, on the other hand, does not automatically mean the claim will be declined. In many cases, it simply means the insurer says there is not enough information yet to commence provisional liability.

💡 To better understand what “reasonably excused” means, refer to our blog When is a claim reasonably excused.

Before Your Claim Is Approved: Provisional Payments

Many workers are surprised to learn that weekly payments can start before the insurer makes a final decision on the claim. Provisional payments exist to reduce stress in the first phase after an injury. They can include weekly payments for lost earnings and payment of medical expenses while the insurer continues its assessment. This helps workers focus on treatment and recovery instead of waiting without support.

If the insurer later declines liability, provisional payments already made do not usually have to be repaid by the worker. That protection is one reason provisional liability is so important in practice

Provisional Payments at a Glance

- They can begin before final claim approval

- They are intended to provide early income support

- They help reduce financial strain in the opening stage of a claim

- Payments already made are generally not repaid if the claim is later declined

How Long Do Workers Compensation Payments Last?

In NSW, weekly payments are available for a maximum of 260 weeks, which is 5 years, under section 39 of the Workers Compensation Act 1987. There are exceptions for workers whose injury results in permanent impairment above 20%.

That does not mean every worker will receive weekly payments for the full period. Duration depends on work capacity, medical evidence, current earnings, and whether the worker continues to meet the statutory requirements at each stage of the claim.

The 130-week point is important because payment entitlement becomes stricter after that stage. Some workers continue receiving payments beyond 130 weeks, but only in limited circumstances and usually with a formal review against the legal criteria.

SIRA also provides a continuation of weekly payments after the 130-week application form, which shows that the period after 130 weeks is a formal decision point, not an automatic extension.

Workers Compensation Payment Periods Explained

A shorter way to understand the workers comp payment schedule is to look at the claim in three stages.

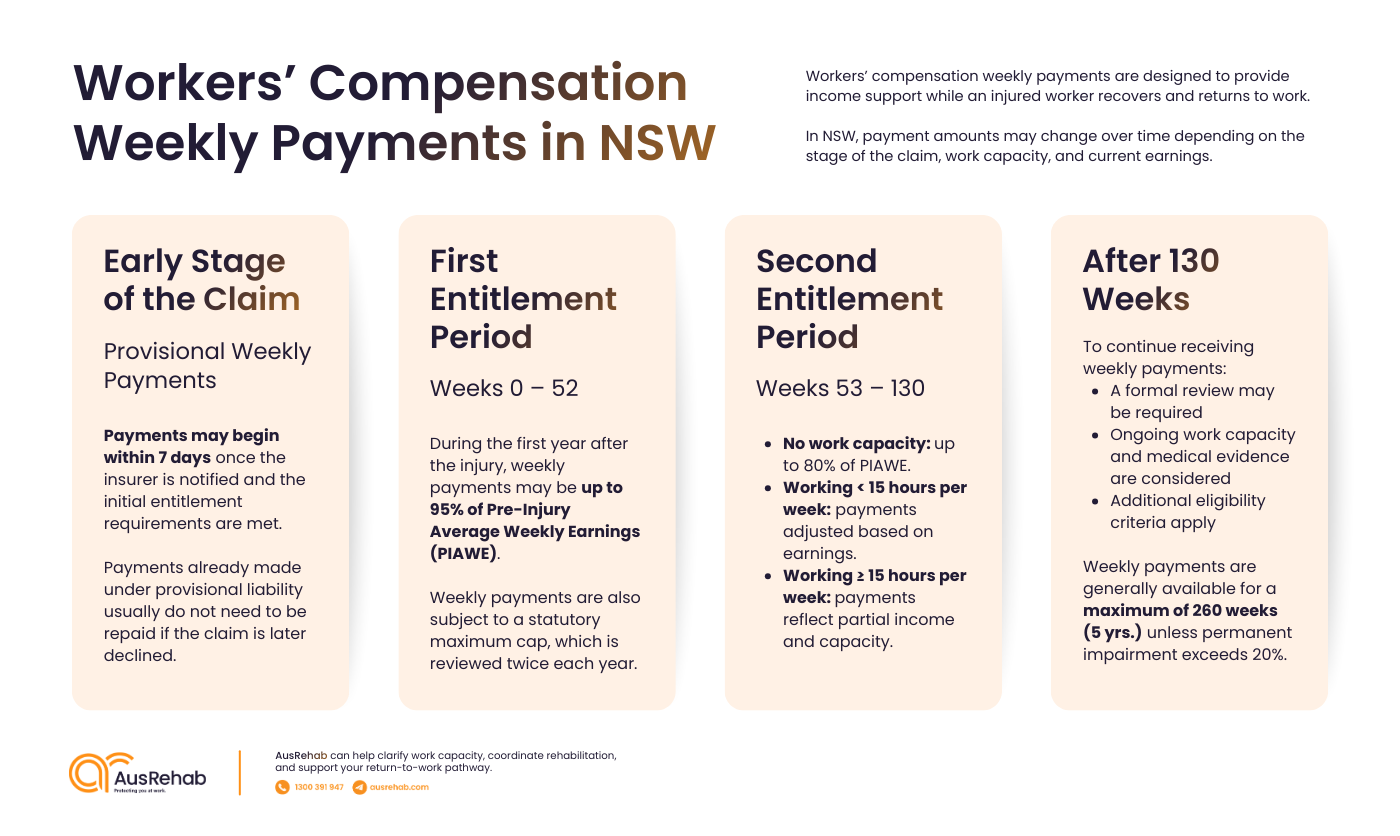

First Entitlement Period: Weeks 0 to 52

This is the earliest entitlement period. It is usually the phase where the worker is most focused on the immediate loss of income, medical treatment, and whether they can return in any capacity.

During the first 52 weeks after your injury, you may receive up to 95% of your Pre-Injury Average Weekly Earnings (PIAWE). This includes regular wages, overtime, shift allowances, and non-monetary benefits (like accommodation or vehicle use).

💡 As of 1 October 2025 to 31 March 2026, the maximum weekly compensation is capped at $2,604.80. This amount is reviewed and adjusted twice a year — on 1 April and 1 October. (Source: iCare weekly payments.)

Second Entitlement Period: Weeks 53 to 130

This middle period often involves more scrutiny around work capacity and actual earnings. The claim is no longer just about the original injury. It is also about what the worker can now do, what duties are reasonably available, and how that capacity affects weekly benefits.

After 52 weeks, your weekly payments depend on your current work capacity:

- No capacity to work: You’ll receive the lesser of 80% of your PIAWE or the weekly maximum.

- Working less than 15 hours/week: You’ll receive the lesser of 80% of your PIAWE minus your current earnings or the weekly maximum.

- Working at least 15 hours/week: You’ll receive the lesser of 95% of your PIAWE minus current earnings or the weekly cap.

After 130 weeks

After 130 weeks, the rules become more restrictive. This is not the point where every claim ends, but it is often the point where continued entitlement requires closer assessment.

To continue receiving weekly payments beyond 130 weeks of your work injury, you must formally apply to the insurer. Ongoing payments are limited to a maximum of five years, unless you’re assessed with a permanent impairment of over 20%.

How Much Can I Receive?

Weekly payments are generally based on pre-injury average weekly earnings, often called PIAWE. PIAWE is important because it sets the financial baseline for weekly compensation. It is not always identical to the amount that lands in your bank each week because the payment formula also takes into account the stage of the claim, current capacity, actual earnings on suitable duties, and statutory maximums.

A change in payment is often tied to one of four things:

- the claim has moved into a new entitlement period

- the worker has returned to some duties

- earnings have changed

- the statutory cap applies

Why Payments Can Be Delayed or Stopped

Payment delays are frustrating, but there is usually a clear reason behind them. The most common issues are missing documents, outdated certifications, missed appointments, unclear capacity information, and insurer questions about liability or work status. SIRA also makes clear that the Certificate of Capacity is central to decisions about entitlement.

Common Payment Issues

Common Workers Compensation Payment Issues and What to Do

| Issue | Why It Happens | What to Do |

|---|---|---|

| Missing certificate | A current medical certification is needed to assess weekly entitlement | Submit an updated certificate and confirm the dates are current |

| Missed appointment | The insurer or treatment team may need updated information on progress or capacity | Rebook quickly and confirm attendance in writing |

| Capacity identified | Weekly payments may change where the worker is assessed as fit for some duties | Review the decision against the latest medical evidence |

| Insufficient medical evidence | The insurer may say it cannot proceed without clearer clinical information | Ask the treating doctor to provide more specific details |

| Wage or worker status uncertainty | The insurer may be unable to confirm coverage or calculate benefits accurately | Provide payslips, rosters, contracts, or employment records as requested |

| Late injury reporting | Delayed notice can create extra questions around causation and timing | Give a clear account of events and provide supporting documents where possible |

Where a payment stops unexpectedly, the most important step is to identify the trigger quickly. The problem is often easier to address once it has been reduced to a specific issue rather than a general sense that the claim has stalled.

💡 For practical tips on avoiding common mistakes, read our blog on The Dos and Don’ts of Workers Compensation.

How Long Does a Workers Comp Claim Take Overall?

The overall length of a workers compensation claim is usually much longer than the timeframe for the first weekly payment. Early payments are intended to provide immediate support, but the claim itself continues while treatment, rehabilitation, work capacity, and return to work options are assessed.

In practice, the duration of a claim depends on several factors, such as:

- the nature of the injury

- how long does the treatment take

- whether liability is disputed

- the worker’s capacity to return in some form

- whether ongoing weekly payments remain payable under the statutory framework

It is also important to separate payment timing from claim duration. Weekly payments can begin within days where provisional liability applies, but that does not mean the matter is finalised. Equally, a claim that remains under review is not necessarily stalled. It may simply be moving through the normal stages of treatment, evidence gathering, and return to work planning.

💡 A straightforward claim with early recovery may resolve relatively quickly. A more complex matter can continue for many months or longer.

What to Do If Payments Are Delayed

When a payment issue arises, the most useful step is to identify the exact reason. A vague sense that the claim has stalled is less helpful than knowing the insurer is waiting on a certificate, wage records, or clarification from a treating doctor.

Here’s a checklist to help you handle delayed payments:

- Check every insurer request carefully

- Keep certificates current

- Respond promptly to calls, letters, and appointments

- Keep copies of certificates, payslips, reports, and insurer correspondence

- Ask for the exact reason if a payment is delayed

- Clarify whether the issue relates to provisional liability, full liability, work capacity, or missing documents

Family support can also be significant here. A family member may help organise records, monitor deadlines, and ensure important documents are sent and retained. In a stressful claim, that practical support can make a real difference.

How AusRehab Can Help

At AusRehab, we support the practical side of recovery and return to work. Our role is to help bring clarity to a process that often feels disjointed, especially when treatment, work capacity, insurer requirements, and employer expectations are all moving at once.

We work with injured workers, employers, treating practitioners, and insurers to keep everyone focused on the same goal. That includes understanding current capacity, identifying safe and suitable duties, and making sure return-to-work planning reflects the worker’s actual functional ability. When that information is clear, the claim process is usually easier to manage.

Our services include workplace rehabilitation, functional capacity evaluations, medical case conferences, and return-to-work planning. These services help build a clearer picture of what support the worker needs now, what duties may be appropriate, and what barriers are affecting progress.

We do not make decisions about weekly payments. That remains the insurer’s role within the scheme. What we do is help improve the quality of the information around recovery, function, and work capacity. In many cases, that leads to a more coordinated claim process and a steadier path back to work.

Find the Right Support After a Workplace Injury

The longer confusion continues, the harder recovery and return to work can feel. At AusRehab, we help injured workers and employers create a clearer plan, supported by practical rehabilitation services and coordinated return-to-work strategies.

Speak with AusRehab to get the right support in place.

Frequently Asked Questions (FAQs)

How long does a workers' comp claim take to settle?

There is no fixed settlement timeframe across all claims. A matter may remain active for an extended period while treatment continues, work capacity is reviewed, and rehabilitation progresses. Weekly payments often begin much earlier than final resolution.

Can payments start before approval?

Yes. Provisional payments can begin before the insurer reaches a final liability decision. This is one of the features of the NSW system designed to reduce financial pressure in the early claim period.

How long does WorkCover take to reimburse expenses?

There is no single reimbursement timeframe that applies to every claim. Timing usually depends on whether the insurer has received the required invoices, supporting material, and treatment information. Incomplete documentation commonly causes delay.

What happens if payments stop unexpectedly?

An unexpected stoppage usually has a specific cause, such as expired medical certification, a work capacity decision, incomplete information, or a change in entitlement period. The first step is to identify the insurer’s stated reason and compare it against the current evidence.

How can AusRehab help if payments are delayed?

AusRehab can assist by clarifying work capacity, coordinating communication between stakeholders, supporting suitable duties planning, facilitating medical case conferences, and strengthening the return-to-work pathway. That support does not replace the insurer’s decision-making role, but it can reduce confusion and improve the quality of the information being considered.